This is the second part to a three-parts series on the financial planning I've done / will be doing for my 9 months old daughter. Part 1 details how I am saving for her, part 2 describes my attempt at making these monies work, and lastly, part 3 documents the type of insurance coverage she has.

Deciding where to park my daughter's savings is one of the hardest financial decisions for me, mainly because these are not my money, and I really don't wish to "lose" it away for her. Yet, for vehicles that guarantee capital (read: fixed deposits, SSBs), the returns are often so low that I can't convince myself that parking her money there will secure her financial future. Therein lies the dilemma. It's a case of emotions fighting against cognition, the heart fighting against the brain. Truth be told, I am still at a deadlock. I hope that by penning down my thought process here, I will gain more clarity on the best way forward.

I've sourced around and found a few possible places to put the money to work:

- Invest in STI ETF

- Purchase Singapore Savings Bond (SSB)

- Park the money in Child Development Account (CDA)

- Put in fixed deposits

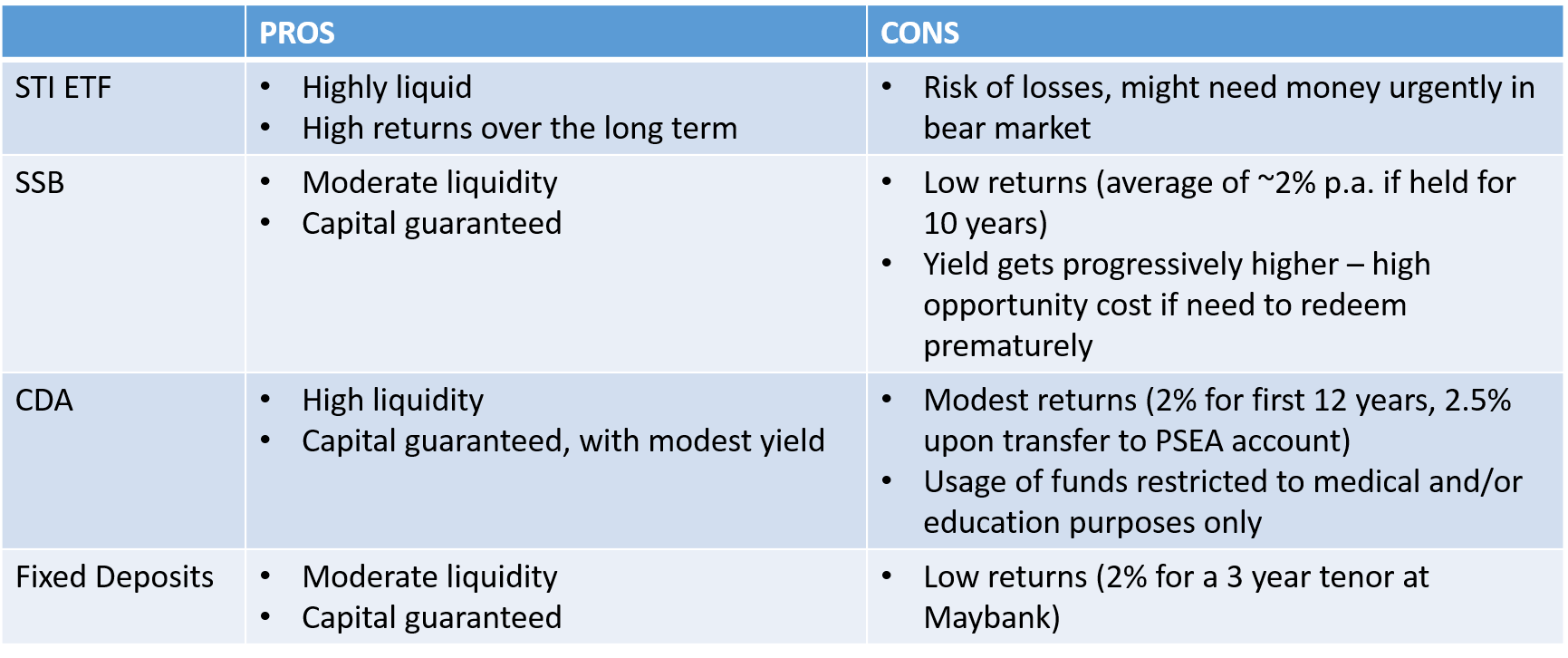

As with everything else, each of them has their own merits and flaws. I attempted to summarise them as shown in the table below:

1. Invest in STI ETF

Over the long term, investing in STI ETF has the greatest chance of yielding the highest return - past 10 year return of ~4% without dividends reinvested, or ~7% with dividends reinvested. It is also highly liquid, as units can be sold in the market anytime we wish. But these are not without risk. Market fluctuates, and although the risk can be minimized over the long term, in the short term, should we need money urgently in a down market, we run the risk of losing part of our initial capital.

2. Purchase Singapore Savings Bond (SSB)

The first few issues of SSB were actually pretty good. I think the average yield if held till maturity was somewhere in the region of 2.5%. However, the yield has been falling, with the latest one in Jun 16 yielding only an average of 1.94% over 10 years. While SSB can be redeemed anytime without risk of losing the initial capital and past interests earned, it is worth noting that the bond is structured in a way that pays bond holders progressively higher interest. This means that the interest in the first few years is low, and should I need to redeem early, my returns might be much lower than the average 10 year yield.

3. Park Money in CDA

The money in CDA can be used at approved institutions (AIs) only. These are mainly for healthcare (e.g. pharmacies; optical shop; payment of medisave-approved private integrated insurance plans) and educational (child care centres; kindergartens) purposes only. More information here. My CDA account with OCBC currently yields 2% p.a. and comes with a NETS card which I can use to make payments at AIs. 2% is not too shabby to be honest, given that I can choose to use the money anytime I wish. Since CDA can be used to pay for healthcare or educational expenses, which is what Emergency funds should be used for anyway, it seems like a good place to park my E. funds. Do note that this flexibility ends on 31 December of the year the child turns 12. All unused funds will be transferred to the child's Post-Secondary Education Account (PSEA), which has an interest rate pegged to the CPF OA account (currently at 2.5%) and higher level of usage restrictions. When the child turns 30, funds in his/her PSEA will be transferred to his/her CPF OA (source), not a bad gift for my child to help her pay for her first house.

4. Fixed Deposits

The most obvious and natural choice, fixed deposit is perhaps the best option for those who wants some liquidity, little chance of losing their capital, and earn some interest in exchange. I think many of the banks, especially smaller foreign banks like CIMB and Maybank are trying to attract more deposits by offering rather high yielding fixed deposits. At the time of writing, CIMB is offering 1.6% p.a. interest for a 6-month tenor, while iSAVvy Time Deposit offered by Maybank is giving up to 2% p.a. if you are willing to lock your money up with them for 3 years. These are great places to park your money for the short term.

So what should I do then? I guess the prudent way is to set aside two different funds - fund A should be highly liquid so it can be used in an emergency, and the other, fund B can be locked up for the long term. The risk/return profile of the two funds should also be opposing in nature - Fund A to be used for emergencies should be capital-guaranteed (low risk), and perhaps a low level of return in exchange for that security; Fund B should aim to have higher return with managed risk.

With these criteria in mind, it becomes quite clear that fund A can only be parked in SSB, CDA or fixed deposits, while fund B should be used to invest in STI ETF which gives substantially highly return compared to the rest. As of now, CDA yields the highest compared to fixed-deposits and SSB, and has no penalty should the money need to be used. Although SSB and fixed deposit is preferred when it comes to how the money can be used, it's less of a concern here since Emergency fund should not be used for frivolous expenses anyway.

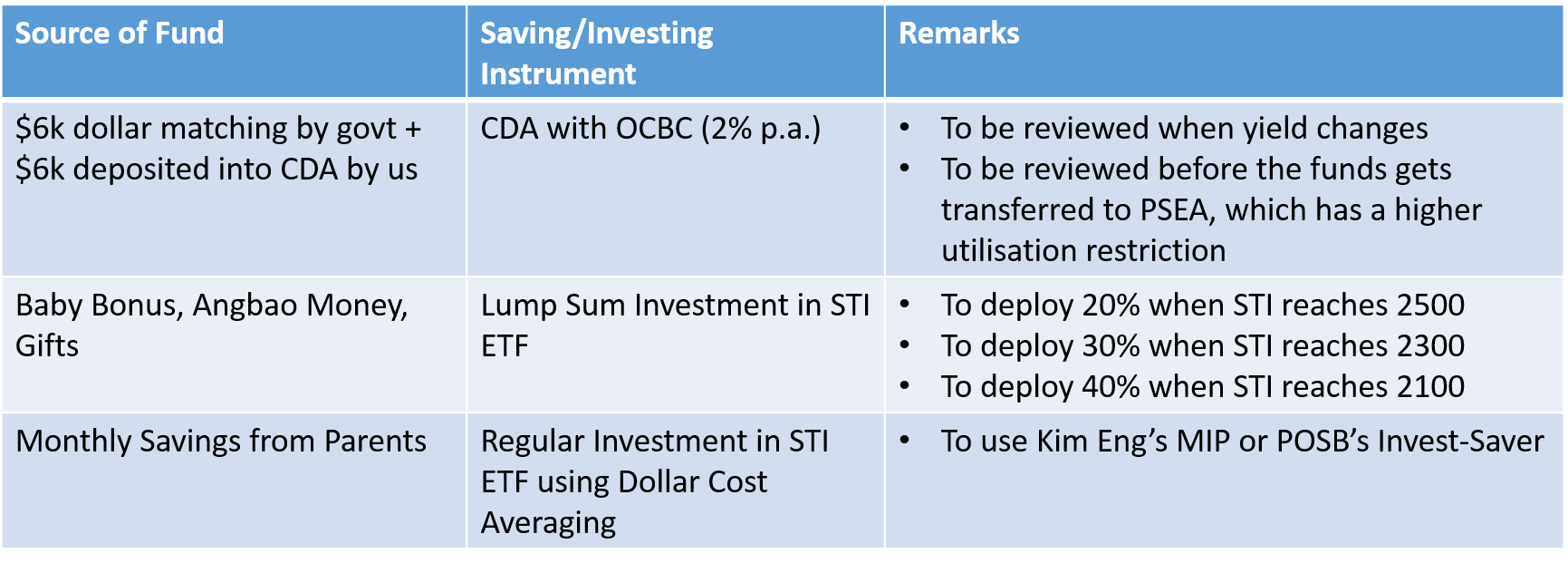

Hence, for now, I shall leave the $12k that's already in CDA as it is as Emergency funds. The Baby Bonus and all the other angbao monies will be used to invest in STI ETF. To be prudent, I will deploy 20% of the savings when STI hits 2500, 30% at 2300, and 40% at 2100. The monthly saving that I am putting aside for her will be used to buy STI ETF using either Kim Eng's Monthly Investment Plan (MIP) or POSB Invest-Saver.

Summarising...

2 comments

commentsImpressed a lot really like your blog.

ReplyThanks for the posting.

Financial planners

What an incredible post it was. Financial planning is much needed approach to have a safe future and glad that you have been doing it for your daughter. We too have twins who are one year old so it would be good to start investing in some good stocks for long term benefits. I am not that educated about wealth management and prefer consulting a certified financial planner india to get started with things.

Reply