Yes! I finally found the exact formula used to calculate the interest rate that the balances in our CPF OA accounts earn. This should be public information, but somehow it took me much effort to find this.

THE FORMULA

The legislated floor rate for OA balances is 2.5% per annum. Since the 3-month average of major local banks' interest rates is lower than this, our OA balances will continue to attract interest at a rate of 2.5% p.a. from 1 Jan 17 to 31 Mar 17.

It's enlightening to know that the OA interest rates is calculated based on 80FD:20SD. I've always thought that only fixed deposit rates are considered.

One thing that is not specified here is the tenor of the fixed deposit. Is it a 12-month fixed deposit, or a 24 month one? I went on to the banks' websites to check it out for myself.

As shown in the above image, 12-month fixed deposit rates for DBS is used for the computation. Cross referencing UOB and OCBC websites yielded the same outcome.

So now we know exactly how CPF OA rates are computed, what does it mean for us then?

WHAT IF INTEREST RATES RISES?

If the computed rates should go above the legislated floor rate of 2.5%, the interest rates on our CPF OA will always be slightly lower than that of a 12-month fixed deposit due to the 80FD:20SD formula. This has a few repercussions:

1.

Paying your home loan earlier than necessary using cash no longer makes financial sense. As the HDB home loan rate is pegged at 0.1% above CPF OA rates, which in turn will always be slightly lower than the 12-month FD rate due to the 80FD:20SD formula, the interest rates on your HDB home loan will be very similar to that of a 12-month FD. Paying down your home loan using cash quicker than necessary no longer makes sense in this situation. If your excess cash is put into a 12-month fixed deposit, the amount of interest earned from this will be very similar (or even higher if you choose a 36-month FD instead) to the interest you could otherwise have saved if the money is used to pay down the home loan. Interest savings is the main reason why we might want to pay down our mortgage early. If this is negated when CPF OA rates rises above the legislated floor rate, it might be wiser to simply leave our excess cash in a FD account to maintain liquidity.

2.

CPF Concessionary Housing Loan will really be concessionary. For the longest time, we wonder how is the home loan offered by HDB

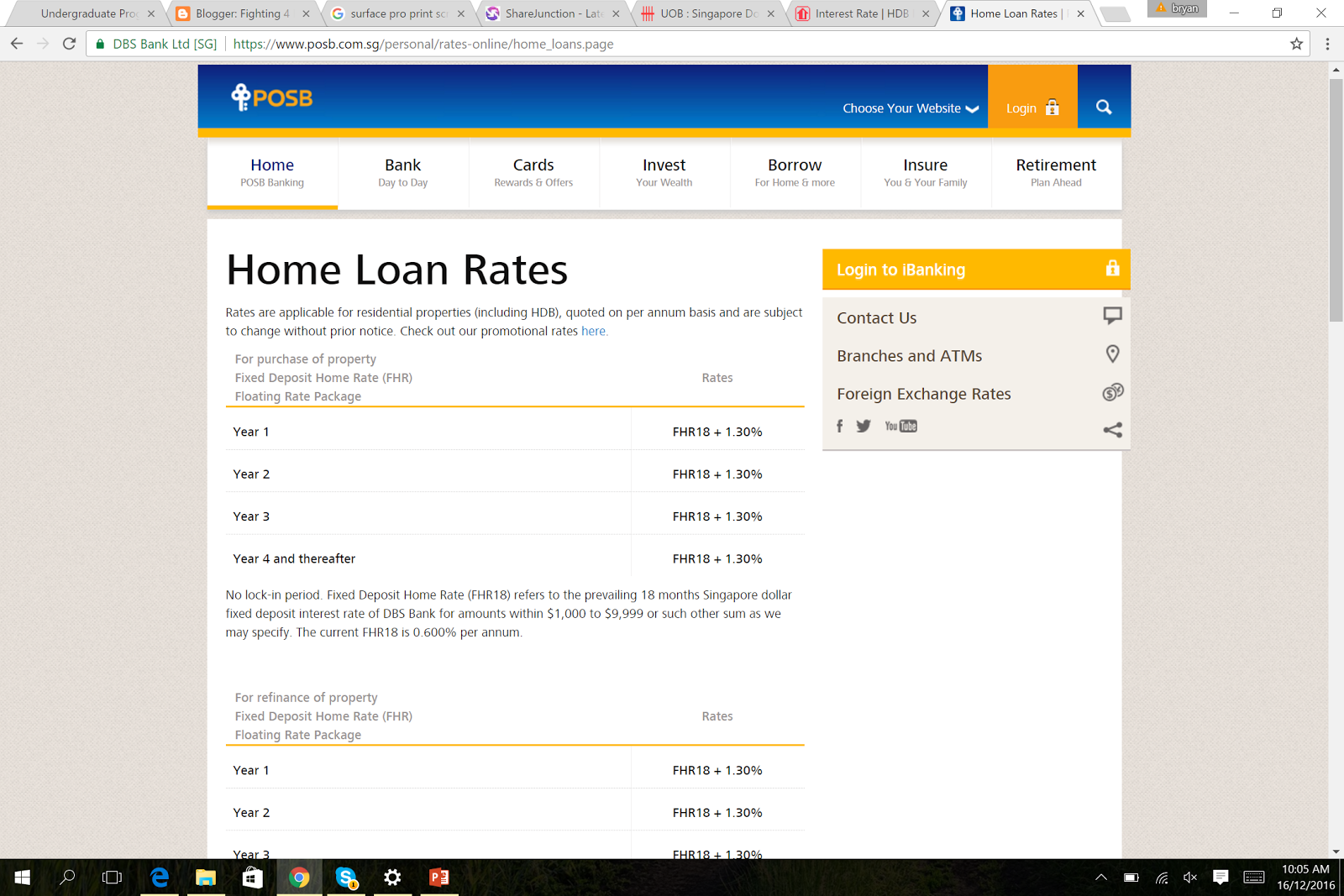

concessionary. Home loan interest rates offered by private banks have been lower than the 2.6% that HDB is charging, and it seems like people who took up HDB loan have been taken for a ride. Further, banks have came up with innovative products that peg mortgage rates to fixed deposit rates, not dissimilar to how OA rates is calculated. While this might provide more stability than products pegged to SIBOR or SOR, they aren't actually better than HDB housing loan in a high interest rate environment. Let's take a look at the FHR mortgage provided by POSB.

The FHR-18 home loan rate is calculated by taking the prevailing 18 months SGD fixed deposit rate offered by DBS bank for amounts within $1,000 to $9,999, and adding 1.30% to it. This is inferior to the HDB loan in a few ways:

- The rates for 18-month fixed deposit is likely to be always higher than the 12-month fixed deposit rates used to compute CPF OA interest. For comparison, the current 18-month fixed deposit rate is 0.60%, as opposed to the 12-month rate of 0.35% (for DBS).

- While the home loan provided by POSB adds 1.30% to the FHR18, HDB only adds 0.10% to the CPF OA rate.

- CPF OA rate takes into account savings deposit rate using the formula: 80FD:20SD. Since SD rates are always lower than FD's, the resulting rates will be lower.

What this means is that once the 18-month fixed deposit rate exceeds 1.30%, interest rate of this particular product will be higher than that of HDB concessionary loan. Now we see how HDB Concessionary Loan gets its name.

3.

Cash will give you higher risk-free returns than balances in CPF OA accounts. Due to the 80FD:20SD formula used to compute CPF OA rates, balances in OA will yield slightly lower returns compared to a pure 12-month FD. The gap will be even wider if you compare to a 36-month FD. Further, cash in FD affords you greater liquidity than balances in CPF OA. There will really be no reason why you would prefer CPF OA over cash parked in FD.

SO WHAT DOES THIS MEAN TO US?

If you expect interest rates to stay long for another decade, then what we have been used to thinking doesn't change. That is, we should continue to:

- choose to take up home loan from banks instead of from HDB.

- pay down our housing loan using cash as fast as we can to save on interest expense

- use cash to make our monthly mortgage payment if you can afford to, and let your OA balances compound (assuming you are only interested in risk-free instruments, so stocks/REITS or other more risky investments are out of your radar)

However, if you think interest rates will rise soon, then we should start questioning the "conventional wisdoms". We've been in a low interest rates environment for far too long, and we are starting to take it for granted. If rates are to rise, we should do the following:

- choose HDB Concessionary Loan over banks' home loans.

- your mortgage loan should stretch out for as long a period of time as

HDB is willing to grant you. Interest

expense incurred can be easily covered by the interest earned from FD.

- use your OA balances for mortgage repayment as much as you can. Keep your cash for FDs, which are likely to earn you more interests, albeit marginally.

ADOPTING A BALANCED APPROACH

The above are some actions that we can take under the two extreme scenarios. However, none of us can predict with certainty what the future might look like. Our best bet is to take a balanced approach and hedge our positions. If you have $100k of excess cash to pay down your mortgage, why not just do $50k first, and keep the remainder as cash just in case? There is no right answer to this really, it depends on what you are comfortable with, and where your conviction lies.

What I hope this article will achieve is to remind all of us that, while we are very used to, in fact,

too used to a low interest environment, there is this other side of the coin that looks vastly different. When we take up a mortgage loan, choose to pay down our loan, and make voluntary contributions to our CPF accounts, we are committing to decision that cannot be easily unwound. It is thus prudent to consider the merits of our choices under different but entirely plausible circumstances, and thereafter calibrate our decisions accordingly.